Many new homebuyers assume that they must work directly with a bank or lender. While working with a bank or other type of lender is an option, it's not always the best one. Working with an independent mortgage broker brings benefits to the table that banks and lenders can’t. Make sure you have all of the information you need before making your decision.

What is an Independent Mortgage Broker? Similar to how knee surgeons are more specialized than general practitioners, mortgage brokers are more specialized in mortgages than bankers. They have direct communication with several wholesale lenders, to whom home buyers do not have direct access. Independent mortgage brokers work as an advocate on the borrower’s behalf and have access to a variety of wholesale lenders to find a mortgage that is custom-fit for you. Mortgage brokers do all of the work, researching all of the products on the market and finding the best ones to meet your needs. Mortgage brokers collect your mortgage application and pass it on to their own portfolio of lenders to get a quote. Why Work With an Independent Mortgage Broker? Brokers provide guidance and expertise throughout the mortgage process and make your life easier by managing the process for you. They also give you a variety of loan options, are licensed in the field, and offer a personalized experience that banks and other lenders can not. 1. Mortgage Brokers give you access to hundreds of different loan options. Most mortgage brokers have experience and relationships with an array of lenders and banks. Not only can this introduce you to lenders that you might not know about, but it may also present you with a wider option of desirable mortgages to choose from. This can save you a ton of time, stress and money by putting qualified and trusted lenders right in front of you from the start. 2. Independent Mortgage Brokers are licensed professionals with unparalleled expertise. Mortgage brokers bring a lot of value to the table. Being independent of a bank or lender allows the broker to “shop” rates for you to find the mortgage that best fits your needs, as brokers have networks consisting of several wholesale mortgage lenders. When you work without a mortgage broker on your side, you are limited to product offerings based only on one particular lender’s products and certifications. 3. Mortgage Brokers provide personal, one-on-one attention. Unlike a bank, which works on specific hours and often requires an appointment, mortgage brokers are there when you need them. When you have a full-time job, kids, and the stress of applying for mortgage loans on your mind, it can make all the difference to have someone work around your schedule. Many mortgage brokers also have systems in place to keep you in the loop and informed throughout the application and loan process. These are only three of the many benefits to using an independent mortgage broker over a bank or other type of lender. Mortgage brokers combine their experience with the ultimate customer service to ensure that you get the mortgage loan you want.

4 Comments

Is it easier today for home buyers with a high debt ratio and subpar credit scores to qualify for a mortgage than it has been in years? And if so, what might that mean for first-time and repeat buyers who are struggling with credit and debt issues but still hope to buy a home?

When the Federal Reserve recently polled senior bank executives on whether they’ve been loosening credit criteria for home-mortgage applicants, most bankers said, “No way, not us.” They’ve kept their rules tight to avoid the problems the lending industry experienced in the housing bust of the past decade. Studies by the Urban Institute’s Housing Finance Policy Center have estimated that lenders’ historically strict underwriting standards have prevented millions of would-be buyers from becoming homeowners. Researchers said that between 2009 and 2014, 5.2 million mortgages were “missing” — that is, they would have been made if lenders had relaxed their tough post-recession requirements. But there’s new statistical evidence that, at least in some areas, standards have been easing. A study conducted by credit-score developer FICO and released in August found that credit scores for new mortgages have been dropping. “As we get further away from the Great Recession,” FICO researchers said, “underwriting criteria seems to have eased and a broader section of consumers are obtaining mortgages as a result.” The study did not specify which type of loans exhibited the most easing. New loans with FICO scores below 700 — including some in the rock-bottom 400s and 500s — have increased from 21.9 percent of the market in 2009 to just under 30 percent (29.7 percent) last year, according to FICO researchers. (FICO scores range from 300, indicating severe credit-history problems and high risk of default, to 850, where the probabilities of missed payments or default are extremely low.) So where has the easing been occurring? Conventional mortgage approval requirements haven’t budged much at the giant investors Fannie Mae and Freddie Mac, both of which were bailed out by the federal government 10 years ago. Although minimum down payments for some borrowers have been reduced in the past two years and debt-ratio rules have been relaxed a smidgen, there has been virtually no decrease in average credit scores for home-purchase loans, according to monthly data compiled by software company Ellie Mae. Nor have there been statistically noteworthy increases in applicants’ average debt ratios at Fannie and Freddie. But loans insured by the Federal Housing Administration appear to be a strikingly different story. From January through March of this year, the average credit score for new-home purchase loans was 672, according to FHA data. By contrast, the average was 701 during the same period in 2011. Refinancings where borrowers replace their existing FHA loans with new ones carried average FICO scores of 709 in mid-2012; earlier this year, that had plummeted to 661. There has also been a big increase in FHA loans with high debt-to-income ratios (DTIs) within the past several years. DTIs are a crucial measure of home buyers’ ability to repay their loans. They weigh monthly household income against ongoing bills for credit cards, auto loans, personal loans and other obligations such as child support and alimony, plus mortgage payments. The heavier your monthly debt obligations, the more likely you are to go delinquent on your new mortgage. Between January and March of 2018, 1 of every 4 FHA loans had a DTI of more than 50 percent, according to the latest data available from FHA. As recently as 2013, just 12.7 percent of approved new FHA applications carried such a high debt load. In the first quarter of this year, almost 30 percent of new FHA borrowers had DTIs between 43 percent and 50 percent. What does this mean for buyers who can’t meet the credit-score and DTI standards needed for most conventional loans? The good news is that you may have a path to homeownership at FHA. But if your household debts are heavy — especially if they exceed 50 percent of your income — get professional financial-counseling advice before signing up for an FHA loan. Your FICO score may meet FHA’s easing standards and your DTI may pass the test. But if you have to spend half or more of your income on your mortgage and other credit payments, you need to ask: Can we really handle this? 2018 Migration Trends accelerate as more people look to leave Denver, San Francisco, and Los Angeles11/2/2018

As mortgage rates climb, affordability in the most expensive markets has suffered, driving more people to affordable, low-tax inland job centers in states like Florida, Texas and Tennessee.

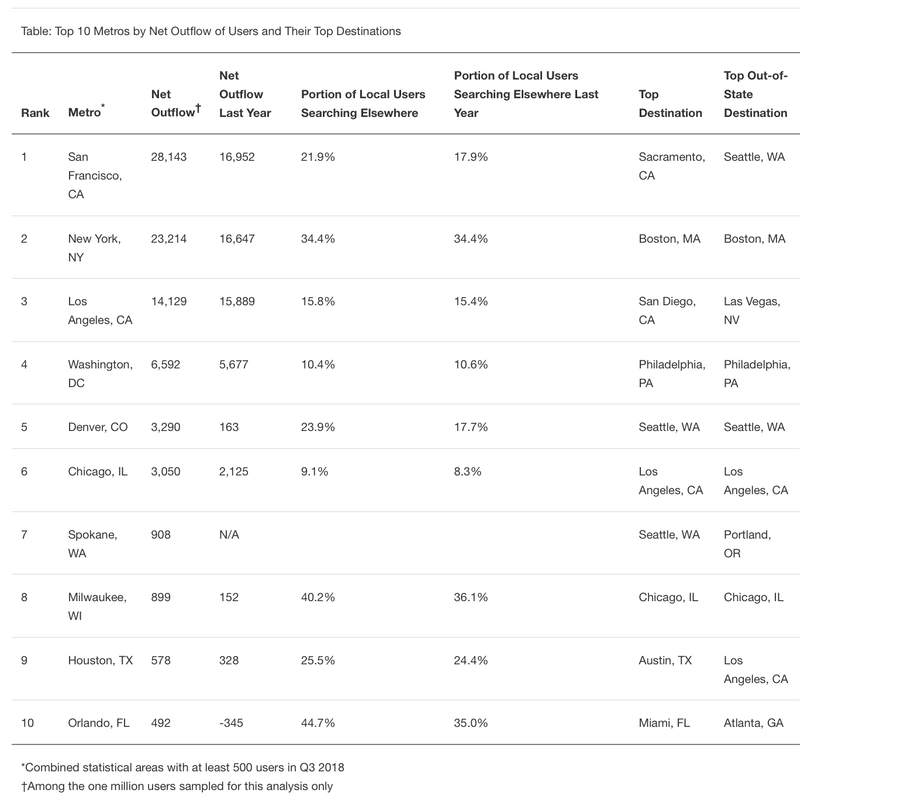

In the third quarter of 2018 people continued to move away from high-cost coastal markets like San Francisco, New York, Los Angeles and Washington, D.C., in increasing numbers. Meanwhile, more affordable areas like Sacramento, Atlanta and Phoenix continued to draw thousands of potential new residents. The latest migration analysis is based on a sample of more than 1 million Redfin.com users who searched for homes across 80 metro areas from July through September. Nationally, 25 percent of Redfin.com home searchers looked to move to another metro area in the third quarter, compared to 22 percent during the same period last year. Affordability continues to be a driving factor causing people to move away from the coasts. “Rising mortgage rates are exacerbating affordability issues that have been driving people out of expensive coastal metros for the past few years,” said Redfin chief economist Daryl Fairweather. “With rates no longer near historic lows, buyers are increasingly cost-conscious, seeking more affordable homes in low-tax states in the South and middle of the country.” Moving Out – Metros with the Highest Net Outflow of Redfin Users:

San Francisco, New York, Los Angeles, Washington, D.C. and Denver posted the highest net outflows in the third quarter. Net outflow is defined as the number of people looking to leave the metro minus the number of people looking to move to the metro. A net outflow means there are more people looking to leave than people looking to move in, while a net inflow means more people are looking to move in than leave.

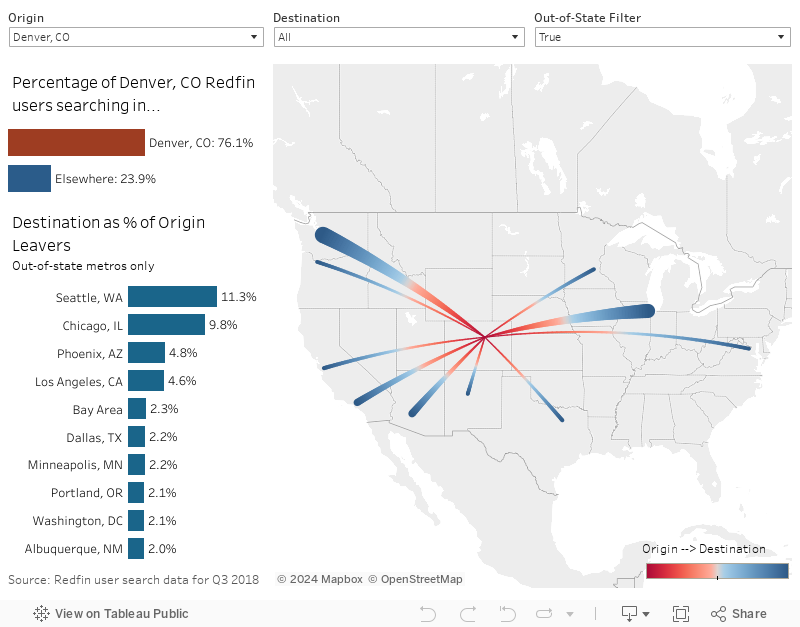

After debuting on the list of top ten metro areas with a net outflow at number seven in the first quarter and moving up to number six in the second quarter, Denver moved up again in the third quarter to pass Chicago at number five. Of all Denverites using Redfin, 24 percent were searching for homes in another metro, up from 17 percent during the same time period a year earlier. Among the Denverites who were searching elsewhere, approximately 23 percent were looking at more affordable metros within the state: Colorado Springs and Fort Collins. A recent New York Times article points out that Denver has suffered from “years of under-building,” and quoted Colorado State University economist Phyllis Resnick as saying that the region’s affordability imbalance may not correct “just through market forces, unless that’s through people moving out.” Of all San Francisco Bay Area residents using Redfin, 22 percent were searching for homes in another metro, up from 18 percent during the same time period a year earlier. Of New Yorkers, 34 percent looked to leave, about the same as last year. Of Los Angelenos, 16 percent looked to leave, compared to 15 percent last year. Moving In – Metros with the Highest Net Inflow of Redfin Users:

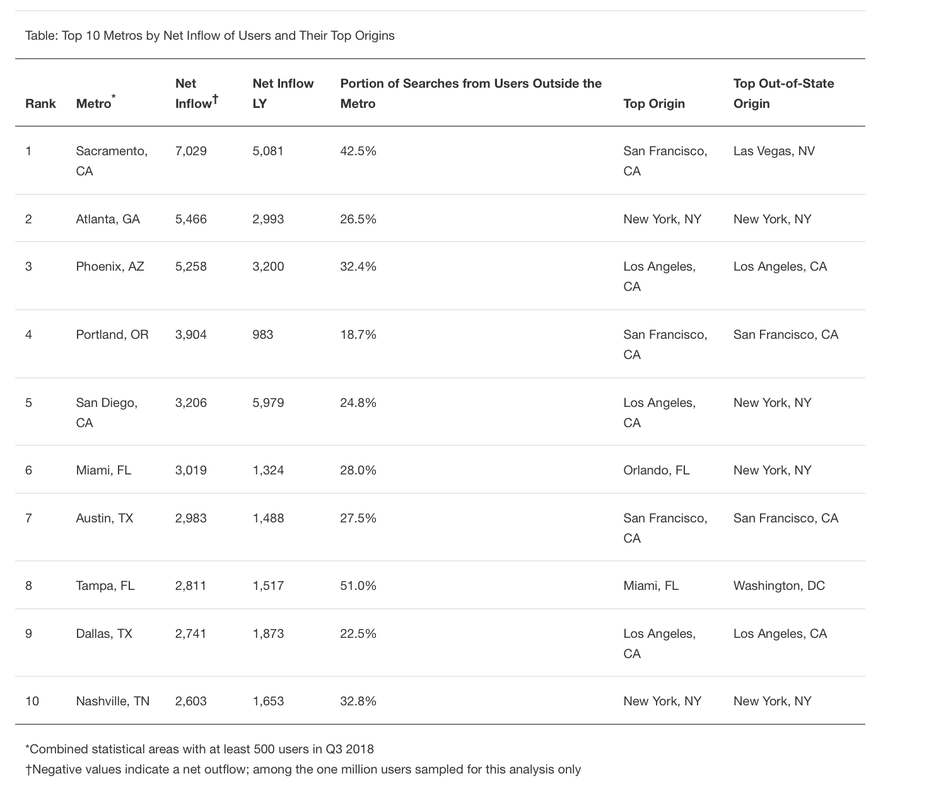

The places attracting the most people are mostly the same regions that have been growing throughout the past year, including Sacramento, Atlanta, Phoenix and Portland. The metro areas seeing the biggest inflows of new residents are the big cities where home prices are still relatively affordable and job markets are strong. Median prices in the metro areas seeing the largest net inflow average around $150,000 below prices in the metro areas with the largest net outflow.

“We talk with a lot of people moving to Atlanta from areas experiencing more of a slowdown, and they seem to think Atlanta is too good to be true,” said Atlanta Redfin agent Ashley Ward. “Benefits of Atlanta that keep drawing people here include top-notch public education, affordable housing, an appreciating market and more job opportunities.”

Methodology

Redfin analyzed a sample of more than 1 million Redfin.com users searching for homes across 75 metro areas from July through September 2018. Users must have viewed at least 10 listings during the quarter. We also excluded locations that in aggregate represented less than 20 percent of a user’s searches. We determined the home metro by mapping the user’s IP address of the most common location they searched from. If a user was searching in more than one metro, we accounted for the share of searches in each metro. Combined Statistical Areas (as defined here) must have had at least 500 users either searching from or in that metro during the quarter. To calculate net inflow and outflow, we take the number of users looking to leave the metro area and subtract the number of users looking to move to the metro area from another metro area. For example, let’s say there are 3,000 people in Phoenix looking at homes outside of Phoenix. 10,000 people outside of Phoenix are looking at homes in Phoenix. More people are moving to Phoenix than moving away, giving Phoenix has a net inflow of 7,000. (10,000 – 3,000 = 7,000) It’s worth noting that net inflow and outflow data does not account for Redfin’s market share or the population of metro areas. In metros where Redfin has a larger number of website visitors, we may have a higher volume of inbound and outbound searches than in metros that are smaller or where Redfin has a smaller user base. The U.S. Census Bureau measures net migration flows, which is a common practice when analyzing migratory patterns.

Mortgage rate trends are inherently unpredictable — right up there with economic recessions and stock prices. But even non-experts could do a pretty good job guessing where mortgage rates will go for the rest of the year. With a hot economy, an active Federal Reserve, and inflation starting to tick up, mortgage rates would have a really hard time going down. The best we can hope for is that they stay where they are long enough for homebuyers and refinance candidates to lock in. Luckily, 30-year fixed rates are still in the 4s. This was considered an impossible range just a few years ago. Despite incessant rate increases, these rates are somehow still available. Don’t want a rate over 5%? Now could be the time to act. Predictions for October and the rest of 2018 There is no shortage of market-moving news in October. Developments now will impact your ability to buy or refinance this month and in the remainder of the year. Rates forecast at the beginning of the year has pretty much come true. Most major housing and financial authorities predicted rates somewhere between 4.7% and 5.0% for 2018. According to Freddie Mac, the average 30-year fixed rate for an ideal candidate jumped to 4.72% at the end of September. That’s very close to the rough 4.75% rate you get when you average predictions from seven agencies like Realtor.com and the National Association of Home Builders. The good news is that we are not very likely to see any more huge jumps for the remainder of the year if forecasts are accurate. But, we are very likely to see a gradual increase until January 2019, starting the year in the high 4s. Been looking for a good rate on a refinance or home purchase? Now might be the time to lock. The economy appears unstoppable, and that’s bad for rates A hot economy is an enemy to low rates, and there’s little doubt we’re in a hot economy. The unemployment rate is at 3.9%, considered very low. There is now less than one unemployed worker for every available job. Yep, there are now more jobs than workers to fill them. Compare that with 2009, when there were more than 6 unemployed workers for every available job. It’s a “workers market,” and that’s good for people in general, because — just taking a wild guess here — most of us would rather have income than an ultra-low mortgage rate. But it’s not so good for those looking to buy or refinance. Inflation is bad for mortgage rates. The simple equation emerges: hot economy = inflation = higher mortgage rates This worker shortage will eventually lead to inflation as companies pay more to hire and retain workers. These firms then pass on those costs via higher priced products. Higher prices for goods and services is the very definition of inflation. Inflation is bad for mortgage rates. The simple equation emerges: Hot economy = inflation = higher mortgage rates So what’s a home mortgage shopper to do? Simply lock in as soon as you can. We won’t be getting off this economic tour de force for a while. The Fed just hiked rates, and will again in December The most recent meeting of the Federal Open Market Committee (aka “The Fed”) just ended September 26. As everyone expected, the group hiked its benchmark federal funds rate. While the action didn’t directly affect mortgage rates, it did lend to an overall environment of rising rates, which certainly doesn’t help the mortgage rate shopper. And, expect another rate hike in December. Twelve of the 16 Fed meeting participants predict one more hike in 2018. That would make a total of four rate increases this year. Those who are waiting for rates to go down may be sadly disappointed in 2018. However, for those who are willing to wait a bit, many experts are predicting a recession in 2020. Half the economists surveyed in a recent poll by the National Association of Business Economics indicate an oncoming recession. An economic pull-back could prompt the Fed to lower the fed funds rate. The Fed could even make mortgage rates artificially low like it did in the wake of the 2008 crisis. (Many economists believe that the Fed is hiking rates now partially because it needs to cut them if the economy turns south.) For homeowners who just want to refinance, a 2020 rate drop might be worth waiting for. But for a homebuyer, it could backfire. Home prices could be 10 to 20 percent higher by then, negating any rate savings. Think you’ll be buying in the next couple of years? Today’s rates may be the best we see. Mortgage rate trends for the rest of 2018 and 2019 Mortgage rates have already surpassed predictions cast by major housing agencies. Now, the question is, what are these groups forecasting for the remainder of the year? To sum it up, everyone is predicting higher rates. Today’s rate might be as good as we’ll see for years to come. Advice for October 2018 Knowing what will happen in October is only half the battle. As a mortgage rate shopper, now you need to know the best actions to take this month. Don’t automatically dismiss a cash-out refinance Homeowners have racked up a monumental amount of home equity in recent years. According to statistics site Statista, U.S. homeowners are sitting on more than $14 trillion in equity. But they are struggling with how to tap into that equity. A home equity line of credit (HELOC) is fast, convenient, and comes with low closing costs. Most importantly, you don’t have to touch your first mortgage to get one. A cash-out refinance, though, replaces your first mortgage and gives you cash back for the new loan amount that exceeds your old one. That gives you a potentially higher rate, plus additional closing costs. But a cash-out refi limits your exposure to a Federal Reserve that is determined to raise rates. Home equity rates are adjustable and rise every time the Fed hikes rates. A 30-year fixed cash-out loan payment never changes. Consider a scenario where a homeowner needs $50,000 cash. Shortly after taking the HELOC, the Fed hikes rates to 2007 levels. To make matters worse, HELOCs eventually turn into “fully amortizing” loans. When they begin, they often require that only interest is paid. The principal-plus-interest payment at 9% gets pretty steep. But with a cash-out loan, you avoid that risk. You lock in at a certain rate and stay there as long as you keep the loan. So, a HELOC may not be the best home equity tool, after all. Loan product rate updates Many mortgage shoppers don’t realize there are many different types of mortgage rates. But this knowledge can help home buyers and refinancing households find the best value for their situation. Following are updates for specific loan types and their corresponding rates. Conventional loan rates Conventional refinance rates and those for home purchases are still low despite recent increases. According to loan software company Ellie Mae, the 30-year mortgage rate averaged 4.94% in August, the most recent data available. This is slightly higher than Freddie Mac’s 4.72% average because it factors in low credit and low-down-payment conventional loan closings, which tend to come with higher rates. Lower credit score borrowers can use conventional loans, but these loans are more suited for those with decent credit and at least 3% down. Five percent down is preferable due to higher rates that come with lower down payments. Twenty percent of equity is preferred when refinancing. With adequate equity in the home, a conventional refinance can pay off any loan type. Got an Alt-A, subprime, or high-PMI loan? A conventional refi can take care of it. For instance, say you purchased a home three years ago with an FHA loan at 3.5% down. Since then, home values have skyrocketed. You refinance into a conventional loan (because you now have 20% equity) and eliminate FHA mortgage insurance. This could be a savings of hundreds of dollars per month, even if your interest rate goes up. Getting rid of mortgage insurance is a big deal. This mortgage calculator with PMI estimates your current mortgage insurance cost. Enter 20% down to see your new payment without PMI. FHA mortgage rates FHA is currently the go-to program for home buyers who may not qualify for conventional loans. The good news is that you will get a similar rate — or even lower one — with an FHA loan than you will with conventional. Related: Read more about FHA costs and requirements on our FHA loan calculator page. According to loan software company Ellie Mae, which processes more than 3 million loans per year, FHA loan rates averaged 4.95% in August, while conventional loans averaged 4.94%. Another interesting stat from Ellie Mae: About 30% of all FHA loans are issued to applicants with scores below 650. FHA loans come with mortgage insurance. But overall cost is not much more than for conventional loans. A little-known program, called the FHA streamline refinance, lets you convert your current FHA loan into a new one at a lower rate if rates are now lower. An FHA streamline requires no W2s, pay stubs, or tax returns. And you don’t need an appraisal, so home value doesn’t matter. Learn more about the FHA streamline refinance here. VA mortgage rates Homeowners with a VA loan currently are eligible for the ever-popular VA streamline refinance. No income, asset, or appraisal documentation is required. If you’ve experienced a loss of income or diminished savings, a VA streamline can get you into a lower rate and better financial situation. This is true even when you wouldn’t qualify for a standard refinance. But don’t overlook the VA loan for home buying. It requires zero down payment. That means if you have the cash for closing costs, or can get them paid for by the seller, you can buy a home without raising any additional funds. “Don’t overlook the VA loan for home buying. It requires zero down payment.” VA mortgages are offered by local and national lenders, not by the government directly. This public-private partnership gives consumers the best of both worlds: strong government backing and the convenience and speed of a private company. Most lenders will accept scores down to 620, or even lower. Plus, you don’t pay high interest rates for low scores. Quite the contrary, VA loans come with the lowest rates of all loan types according to Ellie Mae. In August, 30-year VA mortgage rates averaged just 4.74% while conventional loans averaged 4.94% Check your monthly payment with this VA loan calculator. There’s incredible value in VA loans. Verify your VA loan eligibility (Sep 28th, 2018) USDA mortgage rates Like FHA and VA, current USDA loan holders can refinance via a “streamlined” process. With the USDA streamline refinance, you don’t need a new appraisal. You don’t even have to qualify using your current income. The lender will only make sure that you are still within USDA income limits. More about the USDA streamline refinance. Home buyers are also learning the benefits of the USDA loan program for home buying. No down payment is required, and rates are ultra-low. Home payments can be even lower than rent payments, as this USDA loan calculator shows. Qualification is easier because the government wants to spur homeownership in rural areas. Home buyers might qualify even if they’ve been turned down for another loan type in the past. Verify your USDA loan eligibility (Sep 28th, 2018) Mortgage rates today While a monthly mortgage rate forecast is helpful, it’s important to know that rates change daily. You might get 4.7% today, and 4.8% tomorrow. Many factors alter the direction of current mortgage rates. To get a synopsis of what’s happening today, visit our daily rate update. You will find live rates and lock recommendations. This month’s economic calendar The next thirty days hold no shortage of market-moving news. In general, news that points to a strengthening economy could mean higher rates, while bad news can make rates drop. Tuesday, October 2: Fed Chair Jerome Powell speaks Friday, October 5: Nonfarm Payrolls, wages, unemployment rate Thursday, October 11: Consumer Price Index (a key inflation gauge) Monday, October 15: Retail Sales Wednesday, October 17: Housing Starts Wednesday, October 17: FOMC Minutes Friday, October 19: Existing-Home Sales Wednesday, October 24: New Home Sales Friday, October 26: GDP Now could be the time to lock in a rate in case these events push up rates this month. What are today’s mortgage rates? Despite recent upticks, low mortgage rates are still available. You can get a rate quote within minutes over the phone or online, with just a few simple steps to start. It's not just about getting a lower rate.

For those looking to buy homes, the most popular way to finance a home purchase is to take out a 30-year mortgage. With mortgage rates having been exceptionally low for years, it's been possible to get extremely attractive monthly payments even on relatively large mortgage loans, and the 30-year term gives homeowners a long time to get their mortgages paid off. Yet what's somewhat surprising is that relatively few people look at an alternative to the 30-year mortgage. A 15-year mortgage requires larger monthly payments, but their interest rates are almost always significantly lower. For instance, right now, a typical 30-year mortgage has an interest rate that's more than half a percentage point higher than what 15-year mortgages charge. Half a percentage point doesn't look like a lot. But when you compare the amount of interest you'll pay on a 15-year mortgage at 4 percent compared to the corresponding amount on a 30-year mortgage at 4.5 percent, the difference is astounding. You actually save twice with a 15-year mortgage. You have a lower rate, but the main reason why you pay so much more interest on a 30-year mortgage is simple: You take twice as long to pay down a 30-year mortgage. For example, on a $200,000 loan, monthly payments on a 30-year mortgage at 4.5 percent will be around $1,010. A 15-year mortgage at 4 percent will have monthly payments of about $1,480. The $470-per-month difference pays down the principal balance on the loan that much faster, and over time, that adds up to massive interest savings. In many real estate markets, prices are too high for many homebuyers to afford a 15-year loan. If you can, however, consider the 15-year option closely. Lower rates and faster payouts will cut the amount of interest that goes to the bank and boost what you keep in your own pocket. As home equity conversion mortgages, also known as reverse mortgages, have grown in popularity in recent years, financial advisors have been employing them as risk- and cash-management tools. New government policy changes, however, may put a crimp in these strategies.

The Department of Health and Urban Development describes the HECM as "FHA's reverse mortgage program that enables you to withdraw a portion of your home's equity." It is for homeowners age 62 or older. In 2010, HUD introduced an HECM option that dropped the large upfront costs of the products, which in turn made them more attractive to use proactively, said John Salter, professor of personal financial planning at Texas Tech University and partner with Evensky & Katz Wealth Management. The HECM is his research specialty. New changes announced by HUD in August and enacted Oct. 2 may make HECMs less attractive, however: Upfront costs are raised to 2 percent of the home's value, up from 0.5 percent. According to Salter, lenders won't be likely to subsidize this much. The principal limit factor (loan-to-value ratio) is lowered, meaning less credit is available. The 1.25 percent fee is now lowered to 0.5 percent. This interest-rate reduction, in turn, lowers ongoing payments; however, it causes the borrower's line of credit to grow more slowly over time, according to Salter. Portfolio strategies Advisors have used reverse mortgages in various ways for portfolio management. Cash management. "I've been recommending 'protective' reverse mortgages for clients who are over 62 and have no mortgages, or very small mortgages," said certified financial planner Mark Wilson, president of Mile Wealth Management. "These can provide a line of credit that's available if ever needed. Setting one up early makes sense because the credit limit will rise over time; if not set up early, the credit amount will also rise, but not as quickly," he added. Reverse mortgages fundamentally provide access to a solidly growing amount of cash, said Tom Davison, Ph.D., CFP, researcher and member of the Funding Longevity Task Force of the American College. "One intuitive method is coordinating draws from investment portfolios and reverse mortgages," he said. "Particularly in the first seven to 10 years of living on a portfolio, avoiding drawing from it in down years can be a big boost to sustaining the portfolio through the rest of your life." Long-term care funding. Sally Long, CFP, principal and wealth manager with Modera Wealth Management, said that an HECM could be a way to fund long-term care expenses for clients who may not qualify for long-term care coverage. "What I find compelling about the HECM for this need is the growth in the line availability along with the feature that doesn't require payments of advances but the ability to do so exists," she said. Reverse mortgage basics: A reverse mortgage, also known as an HECM, for homeowners age 62 or older, must be the only mortgage on the primary home. It can be used to purchase a primary residence. The younger you are, the less you get, because there's more time for the loan to compound, said John Salter, professor of personal finance at Texas Tech University. For example, if you have a $100,000 line of credit, you are getting the same amount whether you are 62 or 82. There are three ways to get money from an HECM (as a percentage of the house value and according to your age): • Line of credit. • Annuitized regular payments. • Lump sum. Using an HECM in this way also eliminates some complex steps with long-term care insurance, such as the initial application, underwriting and final approval for coverage, Long said. It also eliminates the cash flow impact of premium payments and potential premium increases. Delaying Social Security. Another portfolio strategy is to use funds generated from a reverse mortgage to cover life expenses, and thereby delay filing for Social Security benefits. This approach has, however, come under criticism recently from the Consumer Financial Protection Bureau. Recent concerns In August the CFPB issued a brief warning against taking out a reverse mortgage to maximize Social Security benefits. According to the report, the costs of a reverse mortgage can exceed the lifetime benefit of waiting to claim Social Security and decreased home equity limits options to handle future financial needs. Additionally, homeowners wishing to sell their homes after taking out a reverse mortgage are "particularly at risk because the loan balance is likely to grow faster than their home values will appreciate." In response, Davison of the American College said he finds the report to be misleading. "What they don't understand is Social Security," he said. "I frame the Social Security delay strategy primarily as a risk-reduction step, and secondarily as income maximization. "Roughly speaking, if you live to life expectancy, Social Security deferral may be about a break-even," Davison added. "But what if you are among the nearly half the people who live longer than 'expected'?" Anyone not sure they have enough money to live to, say, 95, should consider deferring Social Security, he said. Furthermore, Davison added, the brief assumes the highest possible upfront loan costs and does not reflect the fact that a number of lenders offer credits to reduce the initial costs from what FHA allows. Roughly 98 percent of people want to own a home, according to a recent Bank of the West survey. But coming up with the required funds can be tough — especially for cash-strapped millennials in today’s competitive market.

To finance their purchases, one in three millennial homeowners withdrew money from or took loans against their retirement accounts, according to Bank of the West’s survey of over 600 U.S. adults ages 21-34. Meanwhile, one in five millennials who are planning to buy a home expect to do the same. It’s an “alarming” trend, according to Ryan Bailey, head of Bank of the West’s retail banking group. "Millennials are so eager to become homeowners that some may be inadvertently cutting off their nose to spite their face." He recommends relying on savings rather than dipping into your retirement funds. “Borrowing from your retirement may make sense in special circumstances, but it’s definitely not a recommendation we tell people to do,” Bailey tells CNBC Make It. What’s the problem? If you don't have quite enough saved for your first home, you are allowed to pull money out of your retirement accounts, such as a 401(k) or an IRA. But while dipping into your retirement savings may help you put down a bigger down payment and lower your mortgage rate, it also may mean those savings could experience a long-term setback. Think of it this way: You are not allowed to draw on your future Social Security payments to buy real estate and your grandparents weren't allowed to use their pensions, Colorado-based financial planner Kristin Sullivan tells CNBC Make It. "For millennials, the 401(k) is going to be the major component of their retirement. It is a sacred pact with your older self to take care of that older self," she says. If you can't afford to buy a house without raiding your retirement plan, she adds, you may not be able to afford to be a homeowner at this point. Technically, you can withdraw the money from a Roth IRA if you’ve had one for at least five years: Those under 59 ½ years old can borrow up to $10,000 without penalty if you’re a first-time homebuyer, according to the IRS. And because you’ve already paid taxes on this money, you won’t have to worry about any additional fees. If you’ve been contributing to your Roth IRA for less than five years, you can still pull out up to $10,000 — but you’ll have to pay income taxes on the amount. If you have a 401(k), you’ll want to borrow the money as a loan, rather than taking it outright. Getting the money as a loan (up to 50 percent or $50,000, whichever is lower) helps you to avoid income taxes and a 10 percent early withdrawal penalty. But keep in mind that, as with any loan, you'll have to pay the money back, plus interest. Also, should you fail to pay back the loan on time, you may incur a 10 percent early withdrawal penalty. Worse, the terms of the loan generally require that you keep your current job. If you want to switch or are let go for any reason, the full balance of the loan is typically due within 60 days. “This is even the case if you are fired from your job. You would have to pay back a loan at what may be the most inopportune time,” New York-based financial advisor Paul Tramontozzi tells CNBC Make It. What are the alternatives? Before using retirement savings to purchase a new home, review your current spending. Look for any expenses you can cut to save money. "If someone is contemplating dipping into retirement savings, they likely they haven't been able to save up the required down payment to buy the house in the first place, which likely means they don't have a good handle on their finances to begin with," Illinois-based advisor Stephen Jordan tells CNBC Make It. Millennials should also consider scaling down their home dreams in order to reduce the cost. Take a hard look at your finances so you don’t get in over your head, Danielle Hale, chief economist for Realtor.com, tells CNBC Make It. Just over 40 percent of millennial homeowners said in a recent survey said they had regrets after they purchased because they felt stretched financially. “It takes being honest with yourself when you’re making a home purchase,” she says, adding that you should take advantage of filters on home search sites to make sure you're not shopping for something that's too expensive. “With careful financial planning, millennials can have it all – the dream home today, without compromising their retirement security tomorrow,” Bailey says. The Federal Reserve lifted the federal funds rate on Wednesday by a quarter percentage point to a range of 1.5 percent to 1.75 percent. Two more rate hikes are expected this year. Three are expected in 2019, rather than two as initially projected.

If you’re a homeowner with a fixed-rate mortgage, rest easy. If you’re a homebuyer and are shopping for a fixed-rate loan, don’t panic. But if you have an adjustable-rate mortgage or took out a home equity line of credit, pay close attention. ARMs and HELOCs will be more costlyBorrowers with adjustable-rate mortgages that are past the fixed-rate period or home equity lines of credit can expect to see higher rates very soon. “The Fed hike is the tide that lifts all the short-term interest rate ships,” says Greg McBride, CFA, Bankrate.com’s chief financial analyst. These loans are typically tied to the prime rate. When the federal funds rate changes, the prime rate does as well. That means a quarter-point Fed increase means a quarter-point increase on HELOCs and ARMs within the next couple of statement cycles, McBride says. “Whatever your ARM is pegged to – a one-year Treasury, or Libor – it’s a lot higher now than it was one year ago,” McBride says. “And that means the next payment reset could be a doozy. A lot of ARMs will jump to 4.75 percent or 5 percent this year, but borrowers can refinance into a fixed rate below 4.5 percent.” Rates on longer-term mortgages to gradually riseInterest rates on 15-year and 30-year fixed-rate mortgages don’t move in lock-step with the federal funds rate. These loans are tied to 10-year Treasuries, so borrowers looking to get a 30-year mortgage aren’t directly affected by the latest Fed hike. However, the federal funds rate does contribute to the longer-term trends of the 10-year Treasury, and long-term fixed mortgages as a result. With the Fed predicting five more rate hikes over the next two years, the trend for long-term mortgage rates is up. Some experts predict that the Fed’s rate hikes, along with a strong economy and growing deficits, will push the average 30-year fixed mortgage rate to 5 percent in the next couple of years. It would be the first time it’s hit the 5 percent mark since April 2011, according to Bankrate data. “I do see a 5 percent and even a 6 percent rate coming, a year or two out,” says Susan Wachter, co-director of the Penn Institute for Urban Research and a Wharton professor of real estate and finance. “And that, amazingly enough, takes us back to normal. We’ve been living in a world where mortgage rates have been incredibly low.” Consumers who are on the fence about getting a mortgage should act sooner rather than later to make sure they get the lowest rate possible. Mortgage Rates Make Biggest Jump of the Year

DAILY REAL ESTATE NEWS | FRIDAY, SEPTEMBER 19, 2014 Mortgage rates were on the rise this week, with fixed-rates making the biggest one-week leap so far this year, Freddie Mac reports in its weekly mortgage market survey. Fixed-rate mortgages are now at the highest level since the week ending May 1. Freddie Mac reports the following national averages with mortgage rates for the week ending Sept. 18: • 30-year fixed-rate mortgages: averaged 4.23 percent, with an average 0.5 point, rising from last week’s 4.12 percent average. Last year at this time, 30-year rates averaged 4.50 percent. • 15-year fixed-rate mortgages: averaged 3.37 percent, with an average 0.5 point, rising from last week’s 3.26 percent average. A year ago, 15-year rates averaged 3.54 percent. • 5-year hybrid adjustable-rate mortgages: averaged 3.06 percent, with an average 0.5 point, increasing from last week’s 2.99 percent average. Last year at this time, 5-year ARMs averaged 3.11 percent. • 1-year ARMs: averaged 2.43 percent, with an average 0.4 point, dropping from last week’s 2.45 percent average. A year ago, 1-year ARMs averaged 2.65 percent. Source: Freddie Mac |

RSS Feed

RSS Feed